Economy, the Fed, and Rates…

April 14, 2026

Economic Data & Labor Market

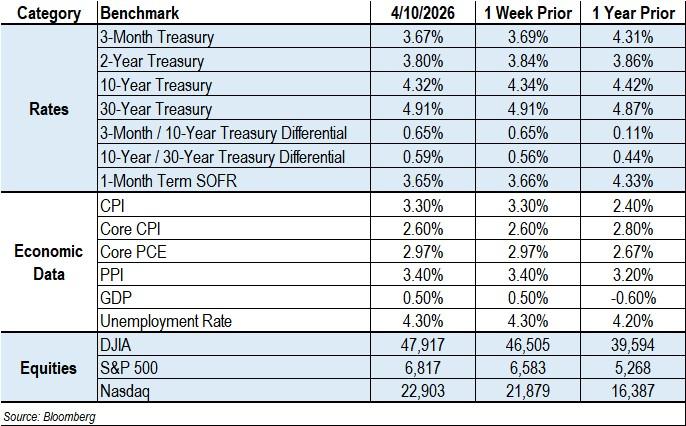

- The first clear household-level inflation print from the Iran war is now in hand. March CPI rose 0.9% m/m and 3.3% y/y, the fastest annual pace since May 2024, with gasoline up 21.2% m/m, its largest monthly increase since at least 1967. Core CPI was firmer and relatively contained at 0.2% m/m and 2.6% y/y, which suggests the shock has hit energy hard first, with broader pass-through still in its early stages.

- Consumer psychology deteriorated sharper than the labor data. The University of Michigan’s preliminary April sentiment index fell to a record-low 47.6 from 53.3 in March. One-year inflation expectations jumped to 4.8% from 3.8%, while long-run expectations edged up to 3.4%. Expectations are worsening faster than payrolls.

- Consumer spending was already soft before the March CPI shock. February real PCE rose only 0.1%, real disposable income fell 0.5%, and the saving rate was 4.0%. Higher fuel costs are acting like a tax, while a shakier stock market threatens the wealth effect that has kept upper-income spending resilient.

- Labor still looks stagnant rather than broken. March payrolls added 178,000, but the six-month trend remains soft, job openings are subdued, hiring is weak, and wage growth has slowed. That leaves the labor market too soft to be reassuring, but not yet weak enough to force the Fed’s hand.

Federal Reserve Policy and the Growth/Inflation Squeeze

- The Fed is still on hold, but the bar for cuts rose again this week. Minutes from the March 17-18, 2026 meeting show policymakers wrestling with both sides of the war shock: most saw a risk that weaker growth and labor-market damage could justify cuts, while many also warned that persistently higher oil prices could require hikes to keep inflation expectations anchored.

- The ceasefire may make short-run easing harder, not easier. If the truce reduces demand-destruction risk more than it removes energy and goods-price pressure, the Fed is left with a milder but more persistent inflation problem. Recession odds fall a bit, but inflation odds do not fall proportionately.

- Policy patience still looks like the base case. The Fed’s public line remains that supply shocks are something policymakers can wait through unless they start to dislodge expectations. The likely path is a hold through most of 2026, with cuts only later if the labor market softens and the war shock rolls off.

Treasury Yields & Bond Markets

- Rates were volatile, but the week ended with a mixed signal rather than a one-way selloff. At the Friday close, the 10-year Treasury yielded 4.32%, the 2-year 3.80%, and the 30-year 4.91%. The 10-year and 2-year were down on the week, while the 30-year was flat, a sign that growth worries partially offset inflation fear in the front and belly of the curve even as the long end stayed sticky.

- March was still a bad month for duration. The Treasury market logged its biggest monthly loss in more than a year. The rates path swung violently over the course of the war. Markets now price less than a one-in-four chance of even a single 25 bp cut in 2026, versus pricing for two cuts before the war began. The message is not conviction; it is a market still toggling between inflation impulse and slowdown risk.

- The cleanest rates takeaway is curve uncertainty, not outright Fed hawkishness. The CPI report did not show major inflation pressure outside energy. Long-end duration still carries a war-risk premium, but the front end has stopped behaving as though hikes are the only plausible path.

Dollar, Commodities & Market Dynamics

- The energy shock remains the macro core. Hormuz remains effectively constrained, with exports running at only 8% of normal, per Goldman Sachs. U.S. crude prices moved from about $70 when the war began to more than $110 in recent weeks, before retracing after the ceasefire.

- This is no longer just a crude-oil story. Refined products and industrial inputs matter more to the real economy than headline crude alone. Diesel, jet fuel, fertilizer, plastics, aluminum, steel, natural gas, and helium are part of the transmission channel, which is why the growth hit can widen even if spot oil stops rising.

- Risk assets have not capitulated, but optimism still looks too strong. Equity analysts continue to expect strong earnings growth, but market pricing and macro conditions suggest more caution is warranted. Earnings expectations still look high relative to the current backdrop.

Policy & Politics: Private Credit Comes onto the Radar

- Fed examining bank exposure to private credit. The Federal Reserve is asking major US banks for details on exposure to private credit funds amid a surge in redemptions and rising troubled loans, with examiners specifically focused on the debt private credit funds have taken on from banks. The Treasury is running a parallel inquiry into insurance company exposure. The $1.8T industry has come under FSOC and FSB scrutiny in recent weeks.

- Dimon warns leveraged-lending losses will exceed expectations. In his annual shareholder letter, Jamie Dimon flagged “modestly weakening” credit standards across the leveraged lending universe, aggressive forward assumptions, weaker covenants, and growing PIK usage, arguing losses in the next credit cycle will be larger than consensus expectations. Dimon stopped short of calling private credit a systemic risk, but cited transparency and valuation concerns.

CRE Finance Market Implications

- Private credit stress is the underappreciated CRE risk. If scrutiny of private credit leads to tighter funding conditions, transitional CRE segments that rely more heavily on non-bank capital could feel it first. Fed and Treasury inquiries into private credit, combined with Dimon’s warning on leveraged lending standards, point to potential tightening.

- Washington’s housing-finance messaging is now part of the rate backdrop. Residential 30-year mortgage rates have climbed back above 6% on rising inflation expectations. With for-sale affordability still strained, the renter-retention dynamic supports multifamily occupancy and pricing power. Pimco made a broader argument that simply ceasing GSE IPO chatter could shave roughly 10 bps off mortgage rates, a useful reminder that policy noise itself carries a risk premium.

Sources: FT, WSJ, Bloomberg, Bloomberg Economics, BLS, BEA, Federal Reserve, University of Michigan Survey of Consumers, Goldman Sachs, JPMorgan annual shareholder letter, PIMCO.

You can download CREFC's one-page MarketMetrics, which includes statistics covering the economy and the CRE debt capital markets, here.

Contact Raj Aidasani (raidasani@crefc.org) with any questions.

Contact

Raj Aidasani

Managing Director, Research

646.884.7566

The information provided herein is general in nature and for educational purposes only. CRE Finance Council makes no representations as to the accuracy, completeness, timeliness, validity, usefulness, or suitability of the information provided. The information should not be relied upon or interpreted as legal, financial, tax, accounting, investment, commercial or other advice, and CRE Finance Council disclaims all liability for any such reliance. © 2026 CRE Finance Council. All rights reserved.