Economy, the Fed, and Rates…

October 21, 2025

Economic Data

- Shutdown distorts the picture: The government shutdown is delaying key releases and, if it persists, could trim roughly 0.1 percentage point of GDP per week, leaving policymakers "semi-blind" on the data.

- Inflation (near-term read): PriceStats points to 0.24% month-over-month for September, lifting the annual pace to 2.66%, the highest since October 2023. The strongest category was household equipment and furniture, now above 5% year-over-year, consistent with tariff costs feeding into prices of import-heavy categories (e.g., furniture, appliances), not local services.

- Labor market is weakening at the margin: Fed Chair Powell said "the downside risks to employment have risen," noting that private-sector gauges and internal research show cooling conditions; ADP estimated companies shed 32,000 jobs in September.

- Growth mix remains uneven: The AI investment boom has supported output, but the expansion is increasingly driven by wealth effects among stock-owning households, while lower-income consumers are being squeezed.

Federal Reserve: Policy Signals & Debate

- Bias toward another cut (Oct 29): Powell said longer-term inflation expectations are "aligned with our 2% goal" and indicated the Fed could halt quantitative tightening "in the coming months."

- "Proceed with care": Governor Christopher Waller backed continued easing but not a larger 50-basis-point move, citing mixed signals on growth and jobs.

- What markets price: Futures imply very high odds of a quarter-point cut on October 29, with debate intensifying beyond year-end as conflicting data and the shutdown muddle visibility.

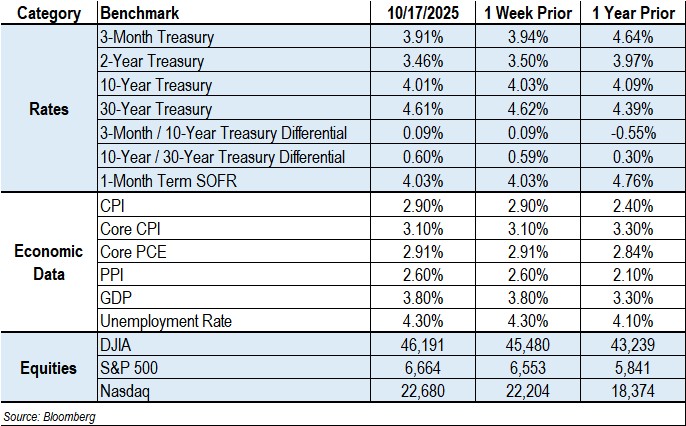

Treasury Yields & Market Dynamics

- 10-year breaks below 4%: The 10-year Treasury yield fell below 4% last week (3.97%), its lowest level since April, driven by regional bank credit concerns and trade tensions, though it later recovered as fears abated.

- Repo market stress emerges: Banks used the Fed’s Standing Repo Facility for more than $15 billion—the largest two-day use since the pandemic—while the overnight repo benchmark (SOFR) printed 4.29% Thursday and 4.30% Friday, briefly above the 4.25% upper bound of the policy range. The episode appears settlement-related and short-lived, but it highlights tighter reserves and supports a slower pace of balance-sheet runoff.

Credit Market Concerns

- Regional bank fraud disclosures: Zions disclosed a $50 million charge-off, and Western Alliance revealed fraud involving commercial real estate loans, with disclosures referencing links to the same borrower group. This triggered a selloff that wiped $100 billion from bank market values on Thursday.

- Dimon's 'cockroach' warning: JPMorgan CEO Jamie Dimon warned "when you see one cockroach, there are probably more," referencing the bank's $170 million hit from Tricolor Holdings' bankruptcy and broader credit concerns.

Implications For the CRE Finance Market

- Rates: A sub-4% ten-year offers a modest boost to fixed-rate financing and valuations. For floating-rate borrowers, the policy path—with another quarter-point cut widely expected—matters more than the long end.

- Liquidity: The spike in standing repo facility usage and Powell's remarks about tightening liquidity argue for closer monitoring of bank capacity for warehouse lines and term lending. If money-market stresses re-emerge, credit spreads could widen and loan closings could slow.

- Renter nation: Renter households rose 2.7% in the year through Q2, compared with almost no growth in homeowner households. Today's young adult is less likely to own a home than in the past, with the median age of a first-time buyer rising to a record 38 in 2024.

- Property-level fundamentals: The renter growth dynamic supports multifamily demand, especially smaller units. At the same time, furniture and materials tariffs can lift turn costs and operating expenses at the margin, which matters for value-add strategies with heavier unit renovation plans.

- Credit quality scrutiny intensifies: The fraud cases at Zions and Western Alliance involving commercial mortgage loans could potentially tighten underwriting standards across the sector.

Go deeper: You can download CREFC’s one-page

MarketMetrics, which includes statistics covering the economy and the CRE debt capital markets,

here.

Contact Raj Aidasani (raidasani@crefc.org) with any questions.