CREFC Capital Markets Update 4/24

April 24, 2023

Slow Issuance Week; Spreads Tighten Further

- Private-Label CMBS and CRE CLOs. No private-label transactions priced last week. However, the pipeline for the remainder of the second quarter (see below) looks promising. Year-to-date private-label CMBS and CRE CLO issuance stood at $9.4 billion, 82% behind last year’s tally at this time of $52.3 billion.

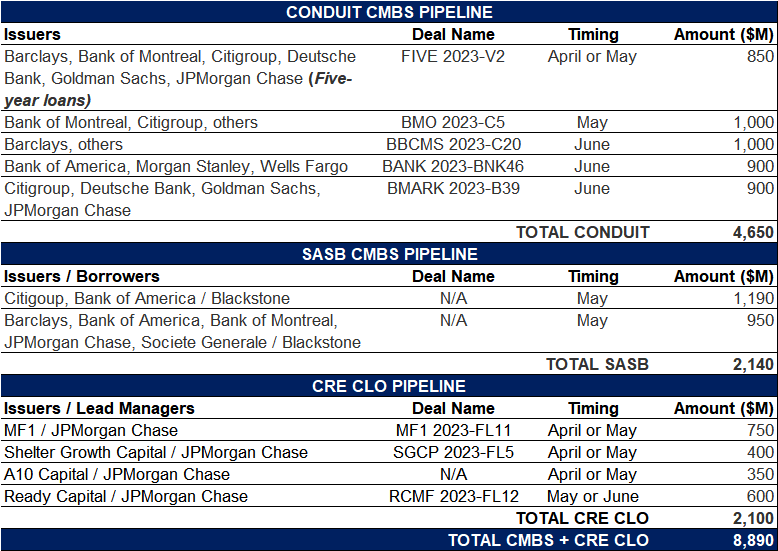

- The forward pipeline for the remainder of the quarter consists of five conduits totaling $4.7 billion, two SASBs totaling $2.1 billion and, in an encouraging sign, four CRE CLOs totaling $2.1 billion. The last CRE CLO to price was in early February, the $534 million ACREC 2023-FL2.

- Benchmark CMBS spreads in the secondary market improved last week, with LCF AAA conduit bond spreads tightening 10 bps to 150. AA spreads were unchanged at 300, while A spreads came in 25 bps to 450 and BBB- spreads were unchanged at 950. SASB spreads tightened ~5 bps to a range of 175 – 265.

- The 10-year Treasury yield was up 6 bps on the week to 3.57%. The yield curve shifted higher as recent comments from Fed speakers reinforced the likelihood of a quarter-point rate increase from the Fed when it meets on May 2 – 3. According to CME’s FedWatch Tool, futures pricing is indicating ~90% probability of a 25-basis-point increase in May, up from ~80% last week. CME 1M Term SOFR rose 8 bps on the week to 4.97%.

- Agency CMBS. Agency issuance totaled $3.2 billion, consisting primarily of a $1.2 billion Freddie K transaction and $1.6 billion in Fannie DUS. Agency issuance for 2023 now stands at $31.8 billion, 42% lower than the $54.8 billion for the same period last year.